By Jim Arnold CEO & Founder of finHealth

In evaluating claim expenditures for large self-insured employers, we often find that errors are made in processing healthcare claims. These “black & white” errors include exceptions such as duplicate payments, medical coding errors, age / gender conflicts, services billed not rendered, payment for non-covered services, improper diagnosis, patients that are no longer eligible for coverage and more. Additionally, we find exceptions where the cost charged to the patient was far beyond a reasonable, competitive rate for that medical treatment. Following are a few examples:

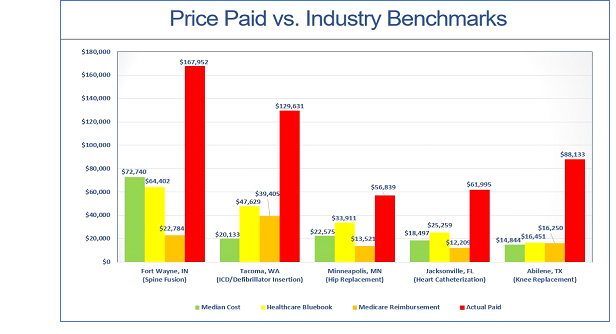

Regarding our chosen benchmarks above, Healthcare Bluebook is calculated based on the collective experience of 400+ self-insured employers as to what is a fair value generally tied to a “care bundle” provided to a patient in a given geography. Medicare benchmarks are far more precise, as these are computed based on that specific hospital’s cost structure, and the billing information associated with diagnoses codes, length of stay, discharge status, amount billed, etc. for that episode of care. The median cost represents the median for that specific medical treatment within that self-insured client’s health plan.

The payers are very protective of the claims data, which actually belongs to you as the sponsor of the self-insured plan, and are generally resistant to having their performance evaluated via a comprehensive audit. This is because it may not reflect well, and they run the risk of exposing certain contracting structures, that while very profitable for them, are not necessarily financially aligned with their self-insured clients.

If the amount charged to a self-insured plan for a given medical treatment is paid at more than 300% of Medicare, we believe that one of the six situations described below has occurred:

In order to help you navigate this potentially contentious landscape with your payer, we have developed a series of questions that we suggest you pose to gain greater insight as to their control procedures, and understand your payer’s level of advocacy on your behalf:

AUDIT / REVIEW

- Are comprehensive audits performed across all claim types, including inpatient, outpatient, emergency room, durable medical equipment, laboratory, pharmacy, etc.?

- How many claims are audited on my company’s behalf each year?

- What percent of my claims processed does that represent?

- What are the criteria used to select the claims?

- How much money was recovered on my behalf from erroneous claims, and what is the breakdown across error type?

- How many claims are audited on my company’s behalf each year?

PROCESSES

- What is your process for validating the “reasonableness” of a provider’s billed charges?

- Do you compare the cost for the treatment or “care bundle” to industry benchmarks to flag aberrant charges?

- At what point compared to a reasonable industry benchmark do you determine the cost is ‘too much’ & take action?

- What actions are taken, and how do you effectively advocate for your self-insured client in these situations to ensure only “reasonable” healthcare expenses are reimbursed?

- Do you compare the cost for the treatment or “care bundle” to industry benchmarks to flag aberrant charges?

- What is your process for reviewing medical records?

- Under what conditions are medical records retrieved to verify the treatment performed?

- Do you deny / reclaim monies when the medical records do not support the charges billed?

- What sanctions are applied to providers that will not produce accurate & complete records, or consistently overbill your self-insured employer clients?

- Under what conditions are medical records retrieved to verify the treatment performed?

Jim Arnold

jarnold@www.finhealth.com / 336-314-9955

Download Article: Are Errors / Excessive Charges Occurring Within My Health Plan?