Simplify & Control Healthcare Costs

What is finHealth’s Primary Value Proposition?

finHealth delivers prevented overpayments / retrospective recoveries that have been inadvertently paid by your third party administrator (TPA). While the TPA has extensive edit capabilities to flag and prevent claim errors, mistakes do inevitably happen. Some of those are related to timing differences in the TPA receiving employee terminations / eligibility data, update timing on contracts, uploading of medical edits to test against procedures and human error. In fact, all of the third party administrators perform multi-pass audits of provider bills on their fully insured health plans, including setting recovery targets to be reclaimed from incorrect billings. Our mission is to equip large self-insured organizations with the capability to flag & recoup these overpayments in real-time versus waiting months / years or forgoing altogether. Additionally, finHealth isolates claims in which the TPA has paid for the procedure at rates significantly in excess of market prices. This command over the healthcare data creates significant leverage for large self-insured employers, and assists in holding your TPA accountable for the accurate & efficient processing of your healthcare claims.

What are the types of errors finHealth finds in analyzing medical claims?

Medical Coding Errors – Medical coding is an incredibly complex discipline. As a doctor performs his or her work in a surgery, their words are transcribed / dictated into a narrative that describes the preparation, the incision / exploration, the revised diagnosis (if different from the preliminary diagnosis), the procedure performed and the resulting outcome. These narratives are then interpreted by a medical coder to translate them into billing codes. Any slight errors in interpreting the narrative can result in a different medical code AND a corresponding different level of reimbursement. Add to that the complex array of network contracts for different health plans, “carve-outs” for certain procedures, the 140,000 unique diagnosis codes, 1.2 million+ medical coding edits and the myriad of codes for surgeries, drugs, medical devices, surgical supplies, prosthetics / orthotics and medical equipment, and you get a sense of its complexity.

Due to this complexity, medical coding edits have been created by the American Medical Association (AMA) in conjunction with the Medicare administration. These edits identify procedures that are not allowed to be billed together due to anatomical reasons (C-section AND a live birth), component procedures that are already included as part of more comprehensive medical procedures, or any set of medical codes that does not conform to current standards of medical care. These errors can all be found by finHealth in real-time, ideally before you reimburse your third-party administrator.

Duplicate Payments – Just like in any Accounts Payable function, duplicate payments can happen. For medical claims this would be the same procedure for the same patient on the same day. In fact, it’s not uncommon to sometimes see claims billed more than twice. This risk has been exacerbated by the rapid consolidation of medical providers and billing systems over the last 10 years.

Eligibility – For any company that has ever performed an eligibility audit, you know full well that there are spouses on your plan that are not spouses and dependents that are not dependents. Maybe it’s the result of a divorce, or a well-meaning uncle trying to get coverage for their nephew? Or maybe it’s an employee taking advantage of the “honor system” that has been in place for as long as employers have had medical plans? Imagine if you could isolate those mistakes / abuses programmatically versus inconveniencing your entire employee population by issuing thousands of verification letters.

How about the situation where one of your employees with healthcare coverage leaves your company to go to work for a competitor? That following week, their $35,000 knee surgery is performed and a claim is filed against your plan using the prior medical policy on file. Depending upon the frequency of eligibility updates from your company and the level of rigor applied by you and/or your third party administrator, these claims may end up being charged against your health plan.

Large Claim Audits – There is a whole another set of medical errors that can only be found by retrieving and examining the original medical records. This detailed audit is OPTIONAL, but confirms whether billed tests were actually requested by the doctor, whether the charges were reasonable based upon the circumstances and additional anomalies relative to misbillings. A thorough internal control system for a large self-insured employer would definitely include a systematic detailed audit of supporting medical records for the largest and riskiest claims paid within the population. In a fully insured plan, the insurance carriers (Aetna, Blue Cross, CIGNA, United Healthcare, etc.) perform three or four passes of audits internally and externally, and set specific targets of $6-10 per member per month in recoveries from the providers for billing errors.

Who are finHealth’s competitors?

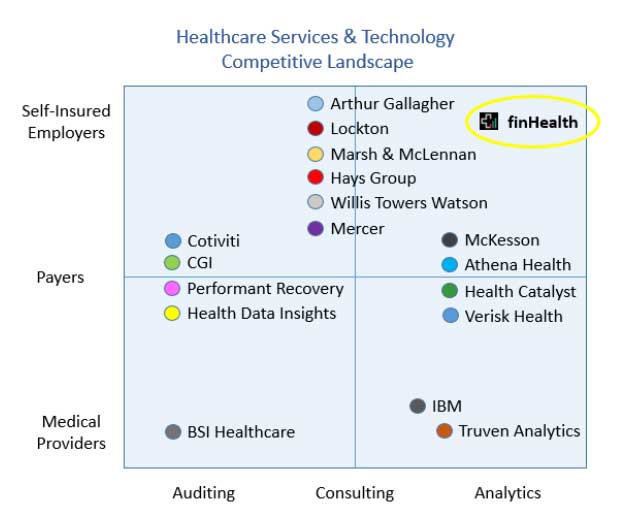

There are a wealth of companies in the healthcare services & technology sector, but they tend to serve different players (health systems, payers & employers) and offer distinct services (audit, consulting & analytics) in the marketplace. This chart lays out the overall dynamics of the sector:

finHealth services & analytics offerings overlap with many of the players in the healthcare space, but our primary value proposition is quite distinct. The common link across our offerings is that we deliver evidence-based analytics to support decisions in optimizing healthcare expenditures. As the main focus, finHealth delivers overpayment prevention / delivered recoveries in real-time to reduce healthcare costs and hold your third party administrator accountable for the efficient processing of your healthcare expenditures. The closest competitors in concept would be medical audit firms that perform a retrospective review of your paid medical claims and/or conduct eligibility audits.

There are at least four national players that perform robust retrospective recovery audits for Medicare (Cotiviti, CGI, Health Data Insights & Performant Recovery) and large payers such as Aetna, Blue Cross & United Healthcare. However, they do not typically engage directly with self-insured employers. Additionally, there are literally hundreds of local and regional medical audit firms, including many that seek to be “best in class” in the various sub-disciplines within healthcare audit. These sub-disciplines include coordination of benefits, subrogation, medical coding, “upcoding”, hospital bill audits, spousal / dependent eligibility and much more.

Conversely, our solution is intended as a real-time vetting of your healthcare claims, ideally prior to the third party administrator (TPA) debiting your account for the funds. We can spot coverage date errors, spousal / dependent eligibility issues, duplicate payments, incorrect medical codes, “upcoding”, medically unlikely edits and more through our highly automated analytic engine. These can be immediately offset against your TPA’s bill. Additionally, we will quantify significant & actionable areas of waste that are currently costing your organization as much as 20-30% of your overall spend that are not adding to patient care. We believe finHealth represents a brand new industry of “healthcare cost governance”, and we have been solicited by the Shared Services & Outsourcing Network to make their community aware of this emerging best practice.

Understand, we are not looking to displace any of the valuable partners already advising you on healthcare benefits. However, there are a number of service providers that are threatened by arming large self-insured organizations directly with powerful healthcare data analytics. At the end of the day, employers provide the patients and health systems provide the care for your employees and their families. The other players in the mix are intermediaries serving as brokers, third party administrators, actuaries, and consultants that might suffer if large corporations are able to make healthcare decisions without them. Already, large players like Boeing, GE, Walmart, Lowes and others are negotiating directly with the health systems.

How do finHealth services fit into our current operational structure with our third party administrator?

Depending upon your billing cycle / debiting of funds from your bank account (usually weekly), finHealth will work with your TPA to set up an automated feed of your medical claims data. As an example, let’s assume you have 10,000 employees with healthcare coverage and another 10,000 spouses & dependents. Your annual expenditures should be somewhere on the order of $130 million annually, and weekly disbursements of about $2.5 million. When you receive that weekly billing for $2.5 million and that corresponding segment of claims data, finHealth will run the claims data through a vetting process to flag claims paid in error. These may be coverage date issues, potential eligibility issues, duplicate payments, medical coding errors, “upcoding”, medically unlikely edits, contract errors and more. These will be flagged, shared with your internal team initially and then presented by finHealth to your third party administrator. We will ask the TPA to process a credit for the errors, and offer any feedback / advice to ensure they are properly processed on a future cycle. finHealth is compensated on those overpayments prevented as well as retrospective recoveries as approved by the client.

What was the catalyst for creating finHealth?

finHealth was founded in 2013 by Jim Arnold to help large self-insured employers safeguard their healthcare expenditures. Prior to finHealth, Jim Arnold founded a company in 1988 that helped large corporations to safeguard their accounts payable spend. Jim built that company up over 25 years (with a great deal of help) into a $50 million+ leading global provider of recovery audit services & solutions. APEX currently serves approximately 35% of the Fortune 100, including organizations like Walmart, Intel, Walt Disney, JP Morgan Chase, Ford, Caterpillar and many more. Many of our client relationships extend 20 years or more.

After leaving APEX, Jim immersed himself in learning web development, significantly different and far more powerful than the programming tools available when APEX was first created. Jim has spent the last 2 and a half years developing a leading edge technology solution that can proudly be put in front of Fortune 100 organizations. Essentially, finHealth Navigator is the product of Jim’s passion to be a trusted advocate for corporations in reducing healthcare costs, while integrating 25 years of best practices in data analytics / payment integrity capabilities. finHealth is now rolling this technology out to the market, looking for thought leaders to partner with us to eliminate the substantial waste in the healthcare supply chain.

How is finHealth compensated for their services and technology solutions?

finHealth offers two basic fee structures to compensate us for our services & technology. The first is our contingent fee recovery model, whereby finHealth receives a fixed percentage of prevented overpayments / delivered recoveries. The fee percentage is inversely correlated to the number of eligible covered lives. All eligible overpayments & recoveries must be agreed to with the client. This model is most appropriate for new clients, as it shifts 100% of the performance risk back to finHealth and eliminates the need to set aside budget dollars to pay for results.

The second option is our subscription model, and is calculated based on a fixed fee per covered life. This structure is most appropriate for organizations that are looking to take advantage of the full range of finHealth’s solution capabilities. As you may be aware, a portion of the dollars we isolate will NOT likely be recoverable (i.e., claims for terminated employees, spousal / dependent eligibility issues and “above market” out-of-network claims), but will make a huge impact moving forward to ensure those errors are not repeated. Under the subscription model, we will load your healthcare data daily / weekly / monthly, flag the overpayment errors, you will resolve them with your third party administrator (with our support & recommendations), and consult with your benefits team as to how to best use the available data to reduce ongoing healthcare costs while also improving employee health outcomes. Additional value adds include prospective cost savings due to improved prices / future cost avoidance (i.e. spouses & dependents removed from your health plan); leverage with your TPA through better command of your data; cloud-based healthcare analytics of your healthcare claims, health assessments and/or fitness tracker data; industry best practices; benchmarking; and our unique Explanation of Benefits (EOB’s) delivered to employees via email.